Although Charles Darwin adopted the term “Survival of the Fittest” from Herbert Spencer to describe his theory of evolution, it is easy to misunderstand if you don’t have context for what “fittest” means. Darwin’s theory of natural selection showed how, in the long run, organisms that could adapt to changes in their environment out-survived organisms that were highly efficient in the current environment but rigid, and slow to adapt.

How is this relevant to loan origination? Few industries exist in an environment that changes as frequently as that of mortgage banking.

Many lenders with what they believe to be a highly-efficient process seek to memorialize that process in their loan origination systems (LOS) through customization – only to find that when they need to upgrade their systems, doing so is time-consuming and difficult.

Too frequently lenders look at the newest release from their LOS vendor and think “how do I get there from here?” How should lenders be thinking about bringing their customizations forward into their new release?

“This porridge is too hot. This Porridge is too cold.” – Goldilocks

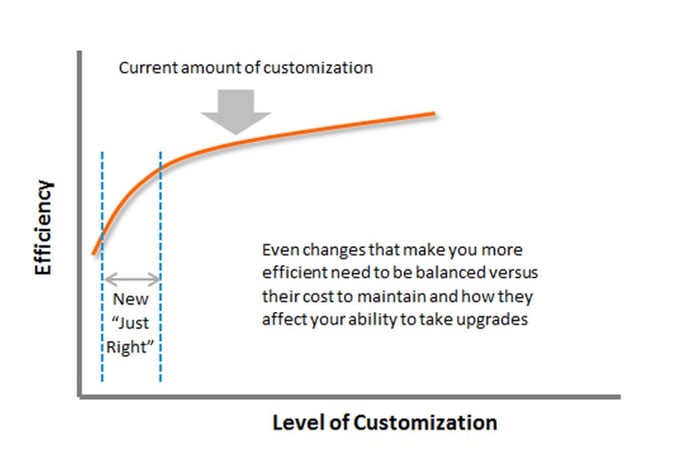

Previously, many lenders defined the ideal LOS as one that was customized to their way of doing business – what was the most efficient at the time. However, the combination of FinTech, new POS technology, the new ULRA, and the constant pace of change are forcing many lenders to take major system upgrades, and to re-think their LOS customization strategy.

Even with some (temporary) regulatory relief, the overall pace of change is speeding up. Many LOS and POS vendors now expect to make a significant release each year, and to continue on that pace, with the requirement that lenders adopt the new releases faster. But that is OK, because the business case for their adoption is growing stronger. Being able to take new releases quickly and easily is the new efficiency.

The best strategy is to make your organization (process, technology and people) as adaptable as possible. How does a lender do that? Although here at CC Pace we help lenders with all three aspects, for the sake of this blog, we will focus on just one: the technology, in this case the LOS.

Typically, the hardest part of taking an upgrade is making sure the customizations survive the transition and associated regression testing.

Therefore, before doing an upgrade, organizations should look at their customizations and determine “given what I know now, and how the package operates out of the box in the latest release, would I make this customization again?”

“Ahhh, this porridge is just right” – Goldilocks

Some Valid Reasons for Customization

- Internal interfaces

- Something particular to your business that is not handled in the package, e.g., a custom funding module

- Support for a different regulatory interpretation (But work hard to see if the vendor’s interpretation isn’t actually acceptable.)

Some Invalid Reasons for Customization

- Low-level users on the project demand a change without regard for the long-term business case (that includes the cost of making and then maintaining the customization). Sometimes even if the change is better, it might not be worth it.

- Exception processing – a mature system (which is typically the type being replaced) will likely have grown to handle exceptions. However, I have seen too many cases where people forget that they are processing exceptions – and let “the rules” pass them by. Focus on getting the straight through process to work.

There is a continuum between a strict “No Customization” policy at one end, and the previous “We bought this system to be able to customize it, let’s do it” at the other.

Goldilocks

An organization should strive for “Goldilocks,” that sweet spot where you implement important customizations, but the rational for the change is made by management, after detailed discussions with the vendor, and performed in a way as to have lower maintenance costs.

If you are one of these lenders with highly customized systems, what is your upgrade strategy?